Are you planning to buy a house and finance it with a mortgage? If so, there are things you must do before applying for a mortgage.

Buying a house is a daunting process that takes a lot of search and time. One of the processes you will go through is the mortgage process. You will need to secure a mortgage from a bank or a financing institution before the sale is finalized.

Before you apply for a mortgage, there are things you should do to increase your approval rate and secure a better rate.

In this article, you are going to learn the top 3 things you should do before applying for a mortgage.

1. Check your credit score

Your credit score will play a vital role when making a purchase on credit. Not only that money lenders will use it to determine your creditworthiness, but also, it will be used to determine the interest on the loan.

A good credit score will increase your approval rate and reduce the interest you pay on the mortgage. The credit score requirements will be different depending on the type of mortgage you are getting and your lender.

According to QuickenLoans, you need a minimum credit score of 620 for a conventional mortgage, 580 for FHA loans, and no minimum score requirements for a VA loan. Some moneylenders require a 620 for VA loans.

Keep in mind that each type of loan requires a different down payment. The following are down payment requirements for all these three loans.

- Conventional mortgages: 20% down payment

- FHA Loans: 3.5% down payment

- VA Loans: According to the U.S Department of Veterans Affairs, there is no down payment requirement for a VA loan. However, you could be asked to pay a one-time fee that helps lower the cost of the loan on taxpayers.

Without a good credit score, you could be denied the mortgage. Even if you qualify for the mortgage, the interest you pay on the mortgage could be too much to bear.

So, before applying for a mortgage, check your credit score. If your credit score is not good or is not within an acceptable limit, consider building it before you send in your mortgage application.

I recommend having a credit score that is at least 740 on the credit score chart. The higher the better.

Is your credit score not good enough? If so, use proper methods to rebuild it.

Your score is wrecked because of decisions you have made in your past life. The good news is that you can rebuild your score. You just need to know the proper methods that will work for you and start working on it.

The following article will walk you through steps you need to take to improve your credit score.

Related: 8 tips you can use to improve your credit score

2. Before applying for a mortgage: Check your income

Just like your credit score, your income will help you seal the deal. If someone is going to lend you hundreds of thousands of dollars in a mortgage, you must prove that you will be able to pay the loan back.

You must have an income that justifies the money you want to borrow.

This is why the lender will need to know:

- How much you make?

- Are you hourly or full-time?

- How long have you been working there?

- Does your spouse works?

- Where does she/he work?

- How long has she/he been working there?

- Etc.

On top of these questions, the lender will need to know if you have other debts. That is:

- Do you have student loans?

- Do you have other mortgages?

- What about car loans?

- etc.

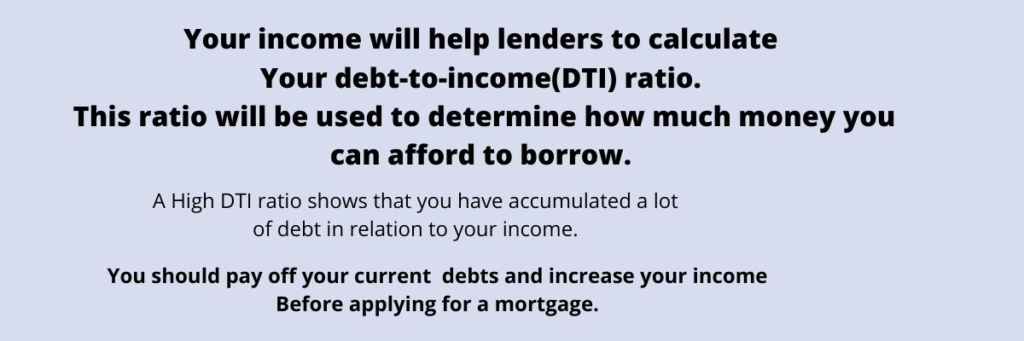

All these questions will help the lender in estimating how much money you can qualify for. In order words, the lender will approve you for the money you can afford to pay back with interest and charges.

Lenders usually calculate your debt-to-income ratio(DTI). A DTI compares the amount of debt you have in relation to your income. A higher ratio will indicate that you have too much debt, and therefore, it would be difficult or impossible for you to afford more debt.

So, even if you have a good income and a good credit score, you could still be denied more loans. Of course, there are some lenders who are willing to take a chance on any borrower.

You must find a way to increase your income before applying for a mortgage. You can increase your income by getting a raise, a bonus, or a promotion at your current job. Use the following article to learn how you can increase your salary.

Is it difficult to get a raise at your current job? Well, there are other ways you can increase your income.

You can get a second job (part-time or a full-time job) or start a side hustle. Whatever works for you, go for it. You can also increase your savings by reducing your debt.

The following articles will give you tips and guidance you need to get your second income figured out.

- 51 easy ways to make money fast

- 20 ways to make money from home

- 8 Reasons you are struggling with money

- Frugal Living: 19 tips that will save you money

3. Before applying for a mortgage: Save for a down payment

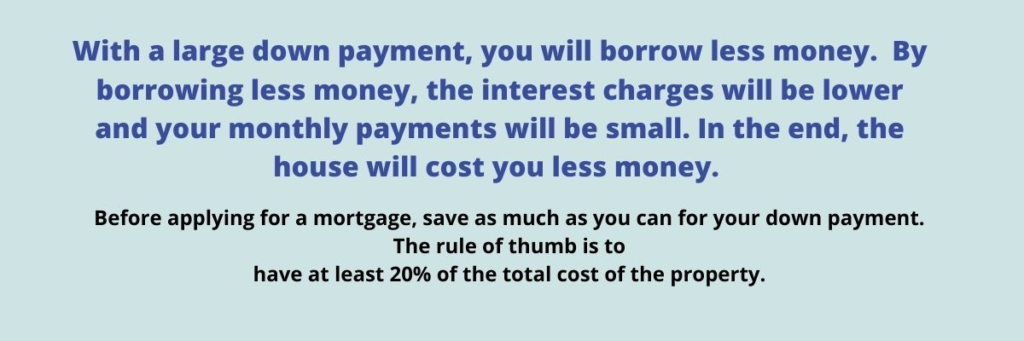

Your down payment will determine whether you get approved or denied. For example, you need a 20% down payment on a conventional mortgage. This means that you are putting down 20% of the total cost and borrowing 80%.

It is always recommended to put down more than 20%. This because, the more you put down, the lesser you borrow. Borrowing less money means that your monthly mortgage payments will be low and you will pay less interest on the mortgage. Furthermore, a higher down payment makes it easy for you to pay off the home much faster.

What if you don’t have a 20% down payment? Some lenders will still give you money. However, you will be required to purchase mortgage insurance. This insurance will protect the lender in case you default on the mortgage.

A low down payment also means that you will borrow more money. Borrowing more money translates to higher interest on the mortgage. In the end, the house will cost you a lot of money that could have been saved.

So, before you apply for a mortgage, make sure that you have saved enough money for your down payment.

If you are having trouble saving money for your down payment, the following article will guide you through every step you need to take.