How to save for a house down payment? Are you trying to buy a house yet struggling with a down payment? If so, this article was written with you in mind. One of the biggest upfront costs is usually the down payment, which accounts for 20% of conventional mortgages. While you can put down a lesser amount and still buy a house, having the required house down payment allows you to lower your monthly payments and avoid private mortgage insurance(PMI).

However, saving 20% of your home purchase is not easy, especially in current markets where inflation has increased the cost of living. According to The Motley Fool, the average home price in the U.S. market is $412,300. So, buying such a house means you need to save $82,460 in down payment. I hate to tell you this, but saving over $80k in a down payment is difficult. That is why most people buy houses without enough down payment, resulting in higher monthly payments due to higher mortgage balances and the extra cost of PMI.

Even if saving for a house down payment is hard, it is still the cheapest way to buy a house as it allows you to borrow less money, avoid higher interest charges, and save money when the house is paid off. In this article, I will walk you through clever tips to save money for a down payment to lower the cost of your house and minimize the risk of foreclosure.

What is a house down payment?

A house down payment is an upfront payment for financing a house with a mortgage. The lender will require this amount, which must be paid in full at closing.

The down payment is a percentage of the total home purchase price. The money you put down becomes your initial equity in the house. However, you can claim it only after paying off your mortgage balance, interest, fees, and other charges required by the lender based on the terms of your contract.

Lenders require a house down payment to help recover some of the loan balance in case you default. The lender will keep the down payment if you cannot afford to pay off the house. In addition to keeping the down payment, the lender will lawfully take the house through foreclosure and sell it at auction. Once the property is in the hands of the lender, it will become a real estate-owned (REO) property.

The down payment will reduce the amount you owe the lender. As a result, you will pay less interest on the mortgage, resulting in a lower monthly payment.

So, how can you save money on a down payment and your home purchase?

Check out these effective money-saving tips if you are looking for easy ways to save for a house down payment. Even on a low income, you can save money for your house purchase using these strategies.

Without further ado, the following are six steps to save for a down payment.

1. Know how much house you can afford

You must first know how much house you need and can afford based on your budget. The house purchase budget represents how much you are willing and able to spend on a house.

This is not the official value of the house you will buy. Instead, it is a rough estimation of what you will spend based on your income, existing expenses, and other financial goals. For example, if you have a good income and don’t want to be in debt for a long time, you can decide how much you are willing to spend on the house, such as $100,000.

This does not mean that you will spend exactly $100,000. It is possible that you will spend a little more or less depending on the market. For example, if you are in a buyer’s market, you will pay less for the house. On the other hand, if you are in a seller’s market, you should expect to spend more money on the house.

After knowing how much you are willing to spend on a house ($100,000 in our case), you will estimate your down payment.

2. Know how much down payment you need

Down payment requirements will vary based on the type of mortgage you are getting. Check out this list of the best mortgages for buying a house.

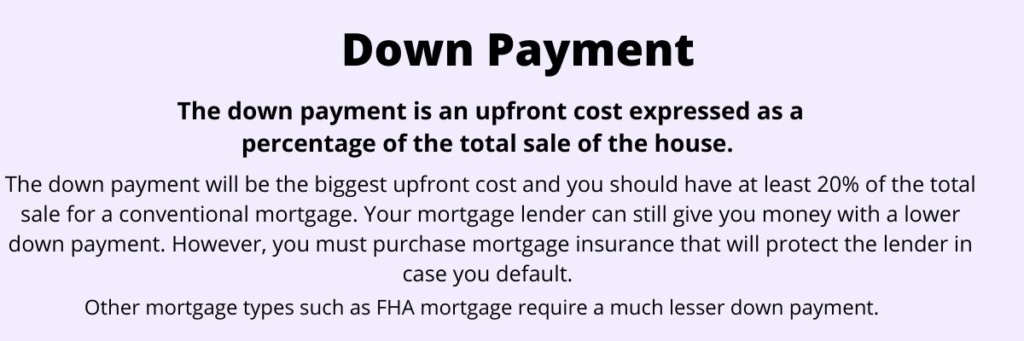

Conventional mortgages require a 20% down payment. As noted by Bankrate, a down payment is a percentage of the total sales of the house that is not financed and is paid upfront. In our example, your estimated down payment would be $20,000 (20% of $100,000).

Other types of mortgages require a different down payment. For example, in our example, you can put down as little as 3.5% on FHA mortgages or $3,500(3.5% of $100,000).

Remember that a small down payment will make you spend more on the house due to higher interest charges. Besides, you must purchase mortgage insurance to protect your lender.

At this point, you know that you need to save at least $20,000 before you buy the house, as shown in our example.

Putting more money down on the house is always a good idea. The more money you put down, the lower the interest charges and, therefore, the lower the monthly payments.

In addition, you must save more than your down payment estimation. This is because there are other costs you will encounter when buying a house. These costs involve but are not limited to mortgage insurance, title search fees, appraisal, inspection, etc.

These costs are known as upfront costs, and they vary depending on the type of mortgage, down payment, and house value.

Read more: What Are The Upfront Costs In Real Estate?

3. How to save for a house down payment: Have a savings plan

Now that you know how much house you can afford and the down payment estimation, you should start saving money. Saving money becomes very complicated for most people because they approach it incorrectly.

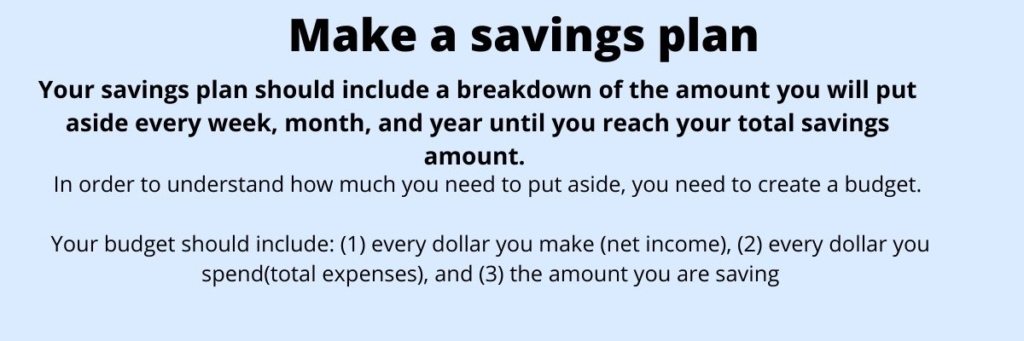

Having a savings plan makes your savings journey easier and possible. Your plan will include the money you can afford to put aside every week, month, or year.

How do you come to this amount?

First, you must know how much you make and where it goes. This is where the budget will come into place. I created a quick guide to creating a personal budget, which you can read before continuing.

The budget will help you estimate an achievable savings rate for your down payment. In addition, the same budget will show you potential areas to cut back and increase your savings.

After knowing every dollar you make and spend, you will decide how much you should allocate toward the down payment every week, month, or year.

For example, let’s say you want to buy a house 5 years from now and should have saved $20,000 in down payment. The following can be a simple breakdown of your savings plan.

- Required down payment in 5 years: $20,000

- Savings requirements per year: $4,000 ($20,000/5)

- Savings Per month: $334 ($4,000/12 months)

- Weekly savings: $83.5 ($334/4 weeks)

4. How to save for a down payment: Cut down your expenses

If the remaining amount after paying your bills does not cover all your savings requirements, you must find other means to save for a down payment.

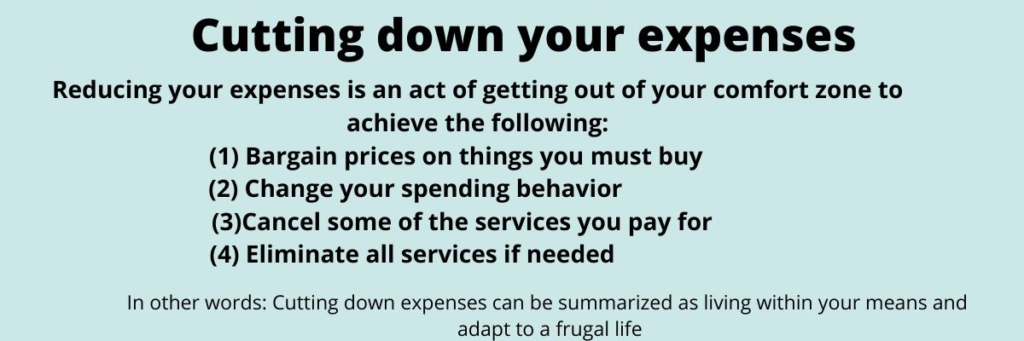

The first thing to do is to cut down your expenses. Look where you spend every dollar and decide where to cut back. The truth is that everything you buy is not essential.

You should always start with things that will not affect your life or loved ones if they are cut or eliminated. For example, if you spend too much on entertainment, consider reducing or canceling them entirely.

Is your apartment costing more than 20% of your income? If so, move into a cheaper area and allocate the saved funds toward your down payment.

Are you spending too much on food, car insurance, books, etc? Find a way to minimize these expenses. Check out the following savings tips and guides to lower your expenses.

- 45 Ways To Save Money On Groceries

- 44 Things You Should Stop Buying To Save Money

- How To Save Money On Car Insurance? 20 Tips

- 16 Ways To Save Money On Utility Bills

5. How to save for a down payment: Get a second job

If you have saved every penny and still haven’t made it, you need to increase your income. There are three ways to do this.

(1) get a promotion/raise/ and bonuses at your current job,

(2) Get a second job, and

(3) Start a side hustle.

All three options are possible if you are willing to adjust your schedule and leave your comfort zone. If you are busy, consider option (1). It could be easier to increase your pay rate than to start a new job or create one.

The following article will teach you step-by-step how to get a promotion, raise, or bonus at work.

You can also get a second job. It does not have to be full-time. For example, you can get a part-time job at your local restaurant in the evening or on the weekend.

If not, consider starting a side hustle. Do you have a ton of clothes that you can sell online? Are you a blogger? Are you good at giving reviews? All these ideas can be turned into side hustles that bring in more than what you are trying to save. The extra cash you make can help you save for a house down payment.

The following articles can walk you through some side hustles you can start today and earn quick cash.

- 49 easy ways to make money fast

- 20 clever ways to make money from home.

- How to make money donating plasma

6. Automate your savings

After figuring out what you will save and how often, you will move to the next step: automating your savings.

Automating savings means the money will automatically be sent to your designated account. If you have a checking account, consider opening a savings account and have money moved there from your checking account.

Having your funds deposited into your savings account directly from your employer is also possible.

By automating your savings, you will avoid forgetting to transfer money, which is a major issue for most people. In addition, the automation will prevent you from postponing the transfer on purpose.