Your payment activities are some of the most important factors lenders consider when evaluating your creditworthiness. You are automatically a risky borrower if you borrow money but can’t repay it. That is why missed payments or late payments affect your credit score negatively. A late payment can drop your credit score by as much as 110 points. According to NerdWallet, late payments stay on your credit reports for 7 years. Late or missed payment’s effect on your credit score fades over time.

This article will explain how late payments affect your credit score and offer tips on keeping your credit history healthy.

How do late payments affect your credit score?

Your payment history is the most significant factor affecting your credit score. Late payments are given higher weight in credit score calculations because late payments lead to defaults, foreclosures, collections, and bankruptcies. All these negative items affect lenders and borrowers financially. That is why your payment history affects your credit score more than any other factor.

How does late payment affect your credit score?

One late payment on your credit report can drop your credit score by as much as 110 points. Consumers with low credit scores lose fewer points from late payments than those with high credit scores.

Additionally, late payments stay on your credit reports for 7 years, hindering your ability to qualify for loans and credit cards. Using your credit accounts responsibly and paying your bills on time can help you recover from a late payment on your credit reports and raise your credit score faster.

Your lenders won’t report late payments to major credit reporting bureaus(Equifax, TransUnion, and Experian) until they are 30 days past due. And the longer you avoid paying it off after 30 days from the due date, the more it will affect your score.

If you recently missed a payment, try to pay it off within 30 days after the due date. You might have to pay some fees and interest charges to your lenders based on the terms of your loans. However, a late payment will not affect your FiCO score or VantageScore if you pay it off before it is reported to major credit reporting agencies.

When is a payment considered late and reported to major credit reporting bureaus?

Typically, a payment is late when it is not made by the due date. However, late does not mean the lender will automatically report to credit reporting agencies.

A loan payment is considered late and reported to credit reporting bureaus only 30 days past the due date. That is when a late payment can affect your credit score. Keep in mind that there are two parties involved in your payments.

- Your lenders. If you miss a payment, you might pay late fees and interest charges based on the terms of your loans. These fees are established based on your financial products, such as a loan, credit card, car loan, mortgage, personal loan, etc. Most lenders charge fees when you don’t make payments by the due date. This fee has nothing to do with your credit score or credit reports.

- Credit reporting bureaus. Credit reporting agencies create your credit reports based on the information they collect from your lenders and other companies that manage your credit accounts. When your payment is 30 days delinquent, your lender will report it to credit bureaus, who will then update your credit reports. A late payment on your credit report will drop your credit score by as much as 110 points. Your credit score will not be affected until a late payment is reported to major credit bureaus.

How do missed and late payments affect your credit score over time?

A one-day late payment won’t hurt your credit score since it will not be reported to major credit bureaus. However, if you continue not to make the payment, your credit score will be affected by missed payments. The following are critical due dates regarding missed and late payments on your credit reports and how your credit score is affected.

- 1- 30 days late payments. Any missed payment won’t hurt your score if you pay it off within this 30-day window. The earlier you pay it off, the better. Delaying your payments to the last day of this window is risky because some of your lenders might have longer processing times.

- 30 – 60 days late payments. Most lenders will report late payments to major credit bureaus after 30 days past due. At this time, your credit score will drop once the late payment is reflected on your credit reports. Any late payments between 30 to 60 days are easier to recover from. The longer you delay paying off late payments, the further they will drop your credit score and affect your health. What you can do at this point is to pay off any late payments or missed payments as soon as possible. You will still lose points on your credit score, but things will get worse if you delay it any further.

- 90 days late payments. Most lenders will disqualify you for loans when you have an outstanding late payment of 90 days on your records. At this time, missed payments can become charge-offs, and your accounts will move into the collection, where collection agencies will attempt to recover the money you did not pay.

How do I know if there is a missed payment on my credit report?

The easiest way to know if there is a late payment on your credit report is to get a copy of your credit report. You can quickly get a free copy of your annual credit report from all three major reporting agencies. Each agency will give you a copy of your annual credit report for free once in 12 months.

After having your report, read it and make sure that the information you have there is current and correct. Any missed or late payments will be included in your report with their corresponding lenders.

You can also check your credit score to see if you have late payments on your report. The easiest place to start is with your lender or credit account issuers, such as credit card providers.

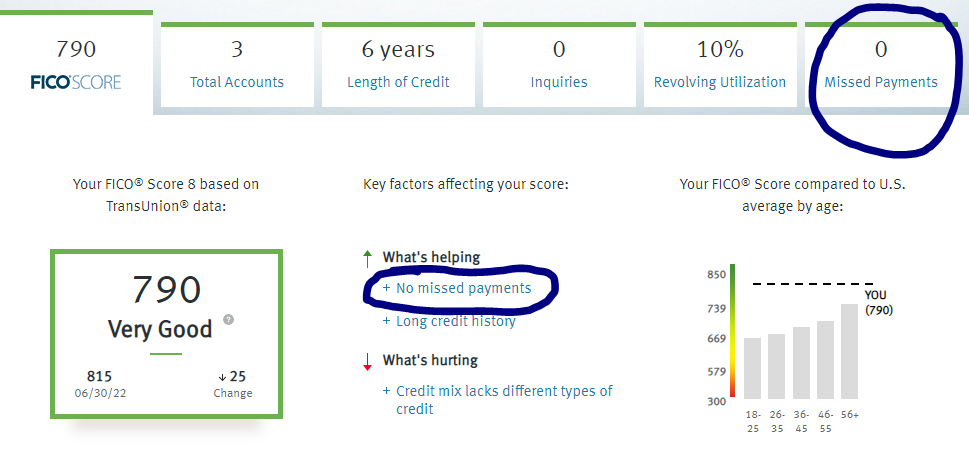

The image above shows that this particular account has zero missed payments. Your online account dashboard will also list any missed payments on the report. In the image above, for example, you can see that our client has 0 missed payments on their credit reports.

How long do late payments stay on the credit report?

Late payments stay on your credit report for 7 years from the original due date of the balance. Late payments will still appear on your report even if you covered your delinquencies. Some accounts and negative information might stay on your credit report for over 7 years. For example, a bankruptcy can stay on your credit report for up to 10 years, whereas collections or charge-offs will stay on your report for 7 years.

How do you avoid late payments on your credit report?

While a late payment will drop your credit score and remain on your credit reports for 7 years, you can quickly rebuild your credit and improve your credit score.

Check out these credit repair tips to raise your credit score after having a late payment on your credit reports.

- Make your payments on time. The first and most important step to avoiding late payments on your credit reports is always to make your payments on time. This is the only way to safely move forward with your accounts and keep your credit history healthy.

- Make your payments before the 30-day window expires. If you missed a payment due to financial setbacks, try to pay it off before it is 30 days past due. Your lenders might charge you fees, but that payment will not be on your credit report if you catch it in that time frame.

- Organize your accounts by due dates and set up reminders. Most people miss payments not because they don’t have the money to pay. Instead, they do not organize their accounts. If you have many credit accounts, organize them by due dates and put them in your calendar. This will help you pay off every single account on time.

- Move your due dates to the same date. One effective method to avoid late payments is to have same-day due dates. For example, you can choose the 15th of each month to be the day you pay off all your accounts. Some lenders and creditors might allow you to change dates if that suits you. Note: Paying off all your bills on the same date could be hard if you don’t have enough cash in your bank account.

- Make more money. If you are missing payments due to no money, a second job can help you meet your financial obligations.

- Use cash only. If you can’t manage your spending behavior, switch to cash only. For example, you can use cash instead of credit cards. This way, you’ll never have to worry about missing a payment if you don’t have balances on your credit cards.

- Do not spend more than you can afford to pay off. Most people use a strategy of leaving below their means to manage their debts and avoid late payments. Spend according to your financial situation, not based on your desires.

The bottom line

A late payment will lower your credit score by up to 110 points and stay on your credit report for 7 years. A one-day late payment, however, will not affect your score as most lenders don’t report late payments to credit reporting agencies until 30 days from the due date.

If you missed a payment, try to make up the payment before the 30-day window elapses. The longer you delay paying off late payment balances, the further they affect your credit score and hurt your credit. Most lenders will not approve you for loans if you have more than 90 days of late payment on your credit reports.

Living below your means is a simple way to avoid late payments. If you have many credit accounts, consider setting up reminders, putting them in your calendar, or having the same-day due date to avoid late payments.